March 21, 2019: from March 21 to 22, 2019, the 2019 Tin Industry chain International Summit hosted by Shanghai Color Network was held in Zhuhai, Guangdong Province. Guo Juan, a senior expert in the Information Center of the Ministry of Land and Resources, analyzed the trends of the global tin mine supply market.

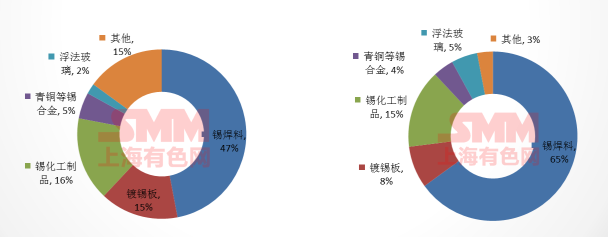

Solder consumption has grown rapidly over the past decade and has replaced tinplate as the largest area of tin consumption. Tin welding is mainly used in the electronic semiconductor industry, although the global electronic components show the characteristics of miniaturization, but the increase of single equipment components does not significantly reduce the total consumption of electronic solder.

In addition to the traditional field, it is expected that more tin will be widely used in modern society as catalytic, sensing, optoelectronic and energy storage materials in the future. At present, many research institutions in the world (especially in China) mainly focus on tin solar film, nano-tin oxide lithium ion battery, tin-based catalytic materials and so on.

Summary of tin mineralization

From the perspective of metallogenic types, there are two main types of tin deposits that have been mined in the world-primary tin and sand tin:

1. The main types of primary tin deposits are as follows:

The main results are as follows: (1) the tin-bearing pegmatite deposit is mainly small and medium-sized, with low tin grade, but the ore is easy to be separated and the recovery rate is high. Mainly distributed in Africa, Brazil, Australia and other places. About 10 per cent of the world's tin production comes from such deposits.

(2) the cassiterite-quartz vein deposits are mainly small and medium-sized, a few large and a few super large. This kind of deposit has high ore grade, easy separation and recovery rate of 70% to 80%. Most deposits can be mined in open pit. Mainly distributed in Southeast Asia and Europe.

(3) cassiterite-sulfide deposits, mostly large and medium-sized, a few super-large. The ore contains 0.2% and 1.5% tin, most of which are underground mining, the mineral processing process is complex, and the recovery rate is low (generally 30% to 60%). Such deposits are mainly distributed in China, Bolivia and the northeast coastal areas of Russia.

2. Sand tin deposits, generally small and medium-sized, but also large and super large. The ore contains 0.05% and 0.3% tin, mostly open mining, the mineral processing process is simple, and the recovery rate is generally 50% to 95%. Mainly distributed in Southeast Asia, Central and South Africa, Australia and other places.

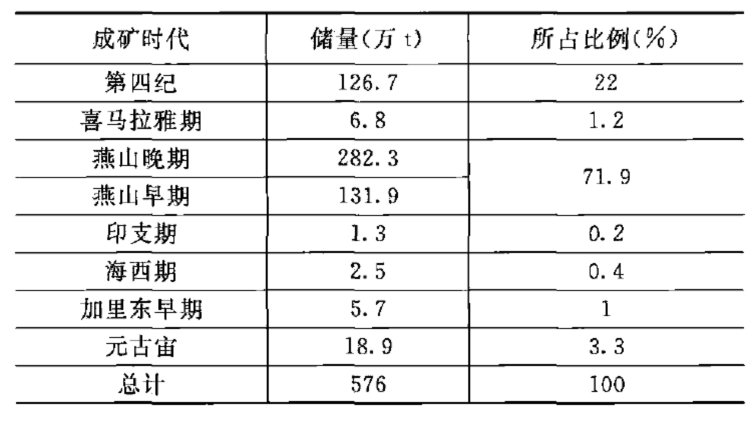

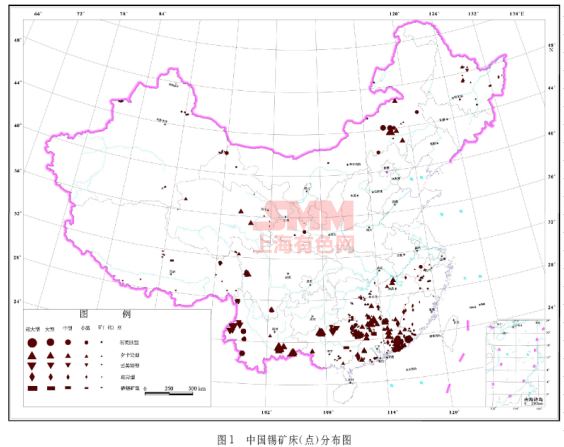

Tin ore resources are characterized by concentrated distribution, complete types, many associated components and dominated by large and medium-sized ones. Tin deposits in China were mainly formed in Yanshan period (71.9%), followed by Quaternary placer deposits (22%). A small amount of tin deposits were also formed in Himalayan (1.2%), Indosinian (0.2%), Hercynian (0.4%), early Caledonian (1%) and Proterozoic (3.3%).

Tin deposits in China are mainly distributed in South China (81.9%) and Southwest China (8.4%).

Development and Utilization of Tin Mine in China

Tin ore is no longer a dominant mineral

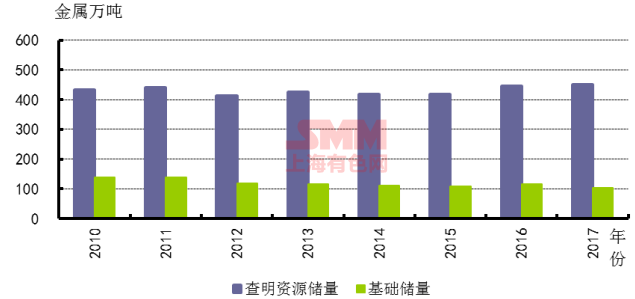

Tin is one of the strategic new minerals in China, which used to be the dominant mineral in China, but the situation is more severe at present. China is the largest tin resource country in the world. In 2018, China's basic tin reserves were 1.1 million tons, accounting for 23% of the world's reserves, ranking first in the world. The tin ore resources in China are highly developed, the reserves are consumed rapidly, the resource advantages no longer exist, the exploitable life of tin ore is insufficient, and the static guarantee life is about 7 years, which is lower than the world level of 12 years (USGS). From 2010 to 2017, the reserves of identified tin deposits in China increased by only 4%, while the basic reserves decreased by 33%.

Variation map of tin reserves:

Distribution of tin deposits in China is concentrated

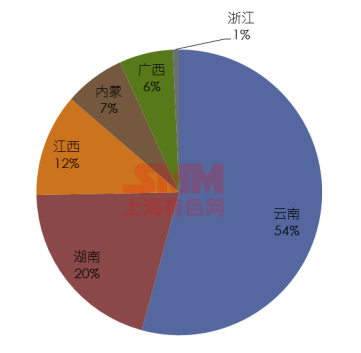

By the end of 2017, 448 tin ore producing areas had been identified and 4.5 million tons of resources had been identified. The basic reserves of the identified resources are 1.04 million tons. Mainly concentrated in Yunnan (29%), Hunan (17%), Guangxi (16%), Guangdong (13%), Inner Mongolia (13%), the above five provinces (regions) tin ore reserves accounted for 88% of the country.

Investment in tin ore exploration in China

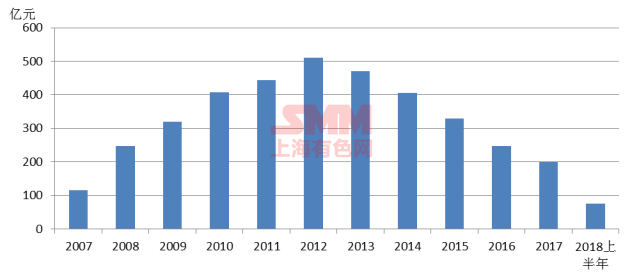

In 2017, China's geological exploration investment continued the downward trend in recent years, with 2012 as the inflection point. The national investment in non-oil and gas geological exploration was 19.8 billion yuan, down 19.8 per cent from the same period last year. In the first half of 2018, non-oil and gas totaled 7.5 billion yuan, a decrease of 7.2 per cent.

As one of the "hardware" (gold, silver, copper, iron, tin), tin ore invests relatively little money in exploration compared with other minerals such as iron, copper, gold and so on. In 2017, 78 million yuan was invested in tin mine exploration, a decrease of 21 percent over the same period last year, accounting for 0.4 percent of the investment in non-oil and gas geological exploration, and the drilling workload was 30,000 meters, down 57 percent from the same period last year.

Comparative map of investment in non-oil and gas geological exploration in China from 2006 to 2017:

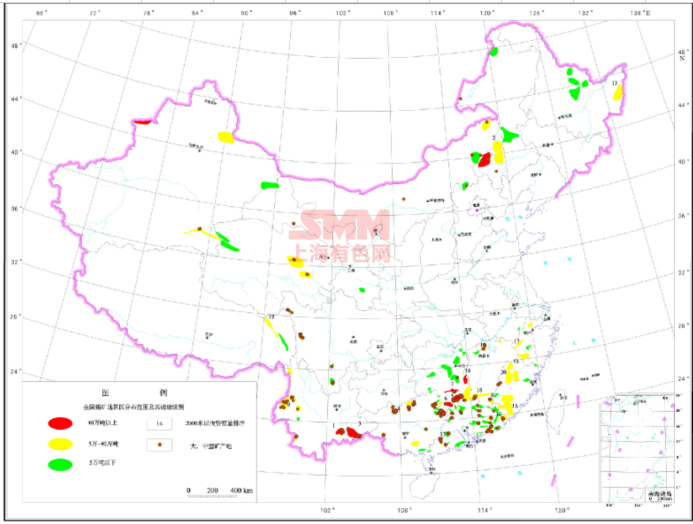

In recent years, there are not many achievements in tin ore exploration in China, there are not many tin metallogenic belts, the lack of major discoveries in recent years, the difficulty of resource allocation is becoming more and more difficult, and the problem of replacement of follow-up resources is prominent. 12th five-year Plan: 10 newly discovered mining areas (5 medium and 5 small). An additional 60,000 tons have been added to the Jiufeng mining area in Hechi City, Guangxi. An additional 60,000 tons have been added to the Velasto mining area in Keshikten Banner, Inner Mongolia. In 2017, a new major tin mining area was added to the tin mine exploration: Wanlongshan large-scale mining area was newly discovered in Dulong exploration area, Maguan County, Yunnan Province, with an additional tin resources of 77000 tons. However, China's tin ore resources have a certain potential, which is more than four times that of the identified resources.

Prediction of tin resources potential in China

The tin ore prediction areas with great potential for tin resources are as follows:

The main results are as follows: (1) Xianghualing-Qianlishan prediction area in Hunan: located in the north of the middle part of Nanling metallogenic belt, the ore-forming geological conditions are superior, the tin ore resources are predicted to be 3 million t, and the main deposit type is skarn tungsten-tin polymetallic deposit. Hunan Tashan-Dayishan prediction area: located in the northern margin of the middle part of Nanling metallogenic belt, the ore-forming conditions are excellent, the predicted tin ore resources are 950000 t, and the main type of deposit is skarn tungsten-tin polymetallic deposit.

(2) Gejiu prediction area in Yunnan: located at the western end of Youjiang metallogenic belt, it belongs to the confluence of Yangtze block, "Sanjiang" arc basin and Nanpanjiang-Youjiang Foreland basin. The ore-forming geological conditions are superior and the tin ore resources are predicted to be 2.22 million t. The main type of deposit is skarn tin-copper polymetallic deposit. The Bazushan-Dulong prediction area of Yunnan Province is located in the western section of the Youjiang metallogenic belt with excellent metallogenic conditions and a predicted tin ore resource of 920000 t. The main type of deposit is skarn tungsten-tin polymetallic deposit.

(3) Huanggangliang prediction area, Inner Mongolia: Xilinhot magmatic arc located in the Daxing'anling arc basin of Tianshan-Xingmeng orogenic belt, the tin ore resources are predicted to be 1.7 million tons, and the main deposit type is skarn iron-tin polymetallic deposit.

Follow-up Resources of Tin deposits in China

It should be pointed out that the grade of reserve tin resources in China is low (mainly between 0.2% and 0.9%). More than 1% of them are only tin polymetallic deposits in Chahe, Sichuan and Xianghualing, Hunan. There are many concomitant components and low comprehensive utilization rate. The comprehensive utilization rate of co-associated tin ore in China is about 40%, and the comprehensive utilization rate of co-associated tin ore is low. Taking Shizhuyuan Mine in Hunan Province as an example, although the deposit is a very large tungsten-tin deposit with 486000 t of tin resources, the tin has not been effectively developed and utilized because of its low tin grade, fine cassiterite particle size and low recovery rate of mineral processing test. Although the Huanggangliang iron-tin deposit in Inner Mongolia has obtained 290000 tons of tin resources, the tin is in the form of colloid and can not be processed mechanically, so it is difficult to be used so far.

Tin ore production in China

China is the largest producer of tin ore in the world, and the output of tin concentrate has been ranked first in the world since 1993. According to the world metal statistics, the output of tin mines in China was 158000 tons (tin content) in 2018, accounting for 41.2% of the world's total output in that year. Yunnan, Guangxi, Hunan, Inner Mongolia and Jiangxi have always been the largest tin production bases in China, accounting for 99% of the output in the five provinces. In 2018, China's refined tin production was 178000 tons, a decrease of 2.4 percent over the previous year, accounting for 48.2 percent of the world's refined tin production that year. Yunnan Tin Group Co., Ltd. and Guangxi Liuzhou Huaxi Group Co., Ltd. are the two largest backbone tin production enterprises in China, which account for about 50% of the national refined tin production. In addition, there are many small companies in Zhejiang, Guangdong and other places, with a production capacity of only a few hundred tons. With the decline of reserves and grade of domestic tin mines year by year, and the increasingly strict management of environmental protection by the state, the supply of tin concentrate continues to be tight.

Provincial statistics of tin production in mines in China:

Regenerated tin in China

There are three kinds of recovery of regenerated tin: (1) tin-containing metal waste is produced in the process of processing, such as tin plate waste, scum, tin-iron alloy slag, etc. (2) tin oxide waste, tin smelting slag and soot are produced in the smelting process. (3) Recycling of waste tin products (such as tinplate, etc.). The recovery and recycling level of waste tin products in China is low. Aluminum, Wuxi steel, glass, paper, plastic and other products can be used as canned packaging materials instead of tinplate. Among them, tin-containing waste has become one of the important supplements to the raw materials of the smelter.

The output of regenerated tin is decreasing. The output of recycled tin in China decreased after it reached a peak of 42000 tons in 2010. This is mainly due to the low price and availability of primary tin mines in Myanmar in recent years, the reduction in the supply of new waste from manufacturing plants and the increasing environmental pressure on smelters. Production in 2017 was 31300 t, accounting for 20 per cent of tin consumption. In the absence of progress in upstream mining, the market expects to adjust the tin supply structure through the improvement of waste recovery, but waste compliance recovery has not become a trend so far, so the current situation of low waste recovery has not changed. In the long run, because of the scarcity of tin resources and the uncertainty of imported raw materials, recycled tin will play a more and more important role in ensuring the supply of domestic tin raw materials in the future.

Development and Utilization of Tin deposits in the World

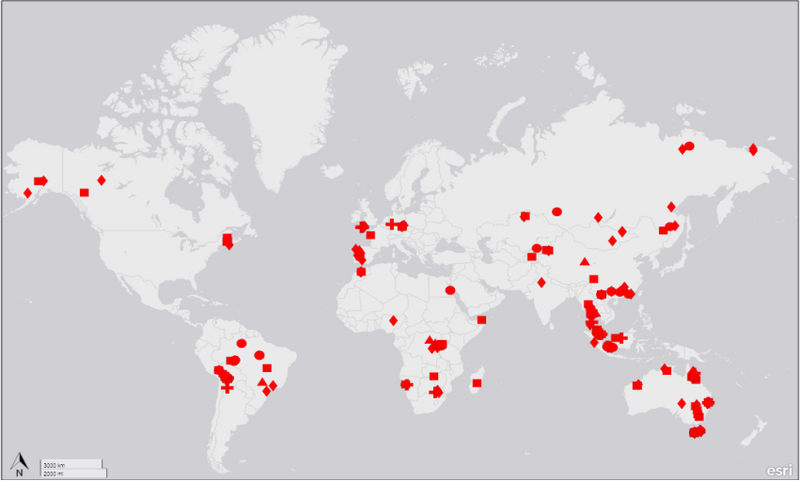

At present, there are more than 70 countries (regions) engaged in the exploration and utilization of tin ore resources in the world, and there are 218 tin mines in the world, including 61 mines with resources greater than 10 000 tons and 16 mines with resources greater than 100000 tons.

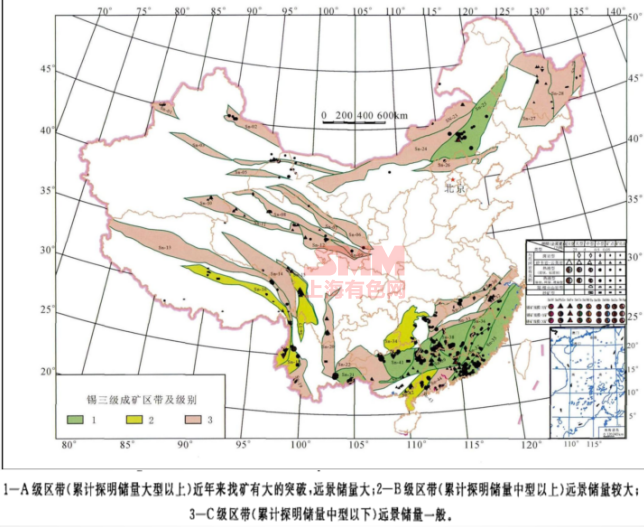

Distribution map of global tin resources:

Tin mine global drilling activities:

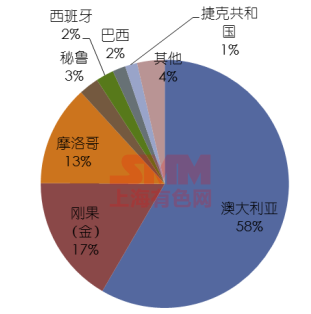

The world is rich in tin resources. According to the estimate of the United States Bureau of Geological Survey, the reserves of tin ore in the world will be 47 billion tons in 2018. The distribution is relatively concentrated. The reserves of China, Indonesia, Brazil, Bolivia, Australia and Russia rank among the top six in the world, with a total reserves of 37.2 billion t, accounting for about 80% of the world's total reserves.

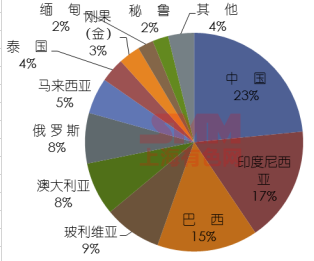

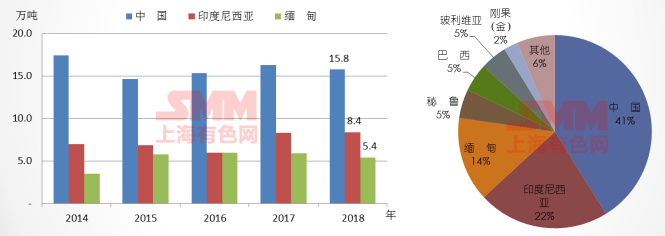

At present, more than 20 countries in the world mine tin mines, and the world tin mine mountain output was 382000 tons (metal volume) in 2018, an increase of 19.1 per cent over the previous year. The main mining tin producing countries in the world are China, Indonesia, Myanmar, Brazil, Peru and Bolivia. in 2018, the tin mine output of more than six countries accounted for 91.3% of the world's total output, with a high concentration.

World tin mine production in 2018

China: it is the largest producer of tin ore in the world. Since 1993, the output of tin concentrate has been ranked first in the world, with a mine output of 158000 tons, accounting for 41% of the world's mine output that year.

Indonesia: it is the second largest producer of tin ore and refined tin in the world. At present, the production of all tin in Indonesia mainly comes from two companies, Tianma (Timah) and Koba (Koba). Tianma Company is the second largest tin production company in the world.

Indonesia's tin reserves, which stood at 800000 tons at the end of 2018, can only last for about 10 years at the current rate of exploitation. In recent years, due to the decline in the grade of tin resources in Indonesia, mining enterprises have been forced to go underground mining, mining costs have increased, and tin production has been greatly reduced. In 2011, tin production was around 100000 tons, which has declined significantly since 2012, falling by 24 per cent to 68000 tons in 2015, and has recovered since 2017, with 84000 tons in 2018.

The Government of Indonesia has imposed a total ban on the export of raw metal mines to increase the added value of the mining industry, and as a result of the new Indonesian tin export and trading regulations, Indonesia has gained greater price control power in August 2013, All exporters are required to trade on the Indonesian Commodity and Derivatives Exchange (ICDX) before exporting; With effect from 1 August 2015, only refined tin ingots, solder and tinplate are allowed to be exported, and exporters are required to issue certificates of export of tin products from government-registered mines.

Indonesia exported 74000 tons of tin in 2018, down 5 per cent from 2017. The decline in exports in 2018 was mainly due to controls on the export of tin ingots from private smelters in the fourth quarter and the suspension of exploration activities, currently only the state-owned Tianma Company can export tin ingots. Thus it can be seen that the policy has a great impact on the import and export trade of tin mines.

Myanmar: the supply of tin concentrate in Myanmar mainly comes from the Manxiang mining area in WA State, which accounts for about 95 per cent of the tin mine supply. After the development of high-grade and low-cost minerals in the Manxiang mining area in WA State, the supply has risen sharply, making Myanmar the third largest supplier of tin mines in the world, from less than 5000 tons in 2012 to 60000 tons in 2016. It fell to 54000 tons in 2018.

Almost all tin mines in the WA region are exported to China in the form of border trade. Imports of tin mines from Myanmar fell in 2018 compared with the same period last year. Myanmar imported 220500 tons in kind in 2018, down 25.4 percent from a year earlier, the lowest in nearly four years.

Specifically, from 2012 to 2015, the mining in this area is open-pit mining of high-grade rich ore, open-pit ore grade is even higher than 10%, the lowest is about 5%; In 2017, it fully entered the stage of underground mining, the grade further dropped to 1.5% and 2%, and the increase in production costs was relatively rapid. In addition, the mining difficulty of the mine has also increased greatly, because after going to the low altitude area, a large number of ores have turned to sulphide ore, high temperature and hot water are great problems, resulting in a significant reduction in the amount of ore mining. However, due to the large number of local mining in previous years, Myanmar has a relatively large stock of ore, which to some extent supports the production of local tin concentrate. There are also some lower-grade mines, less than 3% of which have not been mined in previous years, and the current prices make mining less than 3% of the mines economically valuable, and these mines have been mined so that their total tin exports have not declined.

However, the systematic decline of mine grade in Myanmar is inevitable, and the cost of underground mining continues to rise. The reduction in the production of tin mines in Myanmar will directly affect the import of tin in China. At present, resources can only support Myanmar's output of more than 50,000 tons for less than three years, there is a high probability of decline in the future, and no new resources have been found on the ground. Political instability in Myanmar's WA state will also affect local tin mining, Myanmar tin mine supply worries.

Peru: tin mine production ranks fourth in the world, with a output of 19000 tons in 2018, accounting for 5 per cent of the world's tin production. Minsu of Peru owns the country's only tin mine, the San Raphael mine, which was once one of the few high-grade mines in the world. However, now the problem of grade decline and resource depletion is becoming more and more obvious. Peru's concentrate production has declined year by year in recent years, and tin concentrate production has declined since around 2011. In 2017, Peru's refined tin production dropped to 18000 tons, mainly due to the continuous decline in tin grade at the San Raphael mine in Minsu. In contrast, Tombacca, Minsu's Brazilian subsidiary, saw its refined tin production rise by 12% to 6600t in 2017, mainly due to the treatment of more tin tailings. By the end of 2018, Peru had reserves of about 110000 tons of tin, which could be exploited for about six years.

Brazil: it ranks fifth in the world in terms of production, with a production capacity of 18000 tons in 2018. With a large number of high-grade tin deposits, Brazil's tin mining costs are among the lowest in the world, and most tin mines are profitable even when tin prices are low. Parana Panema (Paranapanema) is the main tin production company in Brazil.

Other countries: in recent years, most producing countries have faced the fact that the grade of their original mines has declined and mining costs have been increasing, such as Malaysia and Bolivia. Although the output of tin mines in Africa (Morocco, Nigeria, Democratic Republic of the Congo), Australia and Brazil may increase to a certain extent in the future, the total output in these areas is relatively low and the impact on our country is limited.

Policies related to the Development and Utilization of Tin deposits: national Mineral Resources Plan (2016-2020), Mineral Resources system Reform, Mineral Resources tax and fee changes

Problems in the Development and Utilization of Tin deposits in China

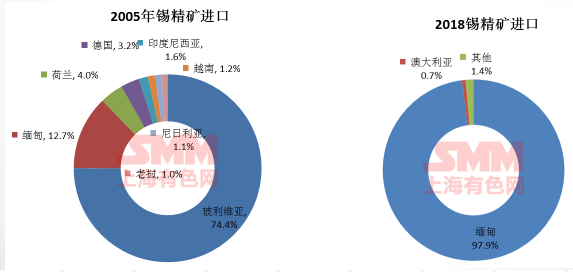

The excessive exploitation of tin resources is serious, and the static guarantee life is limited. China supports 41% of the production with 23% of the world's reserves, and the resources are consumed quickly. The investment of exploration funds is relatively small, the newly identified resources are limited, the import volume is increasing year by year, and the degree of external dependence is increasing. China is the largest importer of tin concentrate, becoming a net importer in 2008, and the import volume has increased significantly year by year. The average import volume of tin ore in China increased 37 times from 0.8000 tons in 2005 to 295000 tons in 2017. 222000 tons (gross weight) in 2018, down 24.9 per cent from a year earlier. At present, the external dependence of China's tin resources is about 25%, and with the growth of domestic demand (peak in 2022) and the continuous dilution of tin resources, the degree of external dependence will continue to rise.

Tin ore imports from a single source. The largest source of imports is Myanmar, accounting for 98% of China's imports, with a small number coming from Australia, Russia, Brazil and Laos. In 2018, China exported nearly three times as much refined tin as it did last year. Customs data show that refined tin exports were 6078 tons in 2018, almost three times the 2175 tons in 2017, mainly due to controls on exports from private smelters in Indonesia, resulting in a continued decline in LME stocks, a stronger price of Rensi and a premium abroad to domestic prices.

Suggestions on the Development and Utilization of Tin deposits in China

We should make an early layout, speed up our efforts to go abroad, and actively explore and exploit overseas tin ore resources. There is a shortage of global resources and a low number of years of security. The import of tin concentrate in China is highly dependent on a single country in Myanmar, but its reserves and grade are declining rapidly, only enough to be exploited for three years. At the same time, the output of the world's major producers of tin resources is unsustainable. Peru also faces a rapid decline in reserves and grade. Indonesia, on the other hand, has been affected by policy and exports have been restricted. In the future, the global supply of tin mines will face a crisis. Go abroad policy environment is good, Belt and Road Initiative, China-Africa cooperation (copper, aluminum, lithium pricing power). It is suggested that the early layout and the allocation of overseas tin resources should focus on Southeast Asia, Africa and South America. Relying on the "Belt and Road Initiative" initiative, cooperation on tin resources projects has been carried out in Myanmar, Indonesia, Australia and other countries. The potential countries of tin resources in South America, such as Bolivia, Peru and Brazil, have maintained good cooperative relations with China, which provides a strong guarantee for Chinese enterprises to carry out tin resources cooperation in the region. The rising production of tin in the Democratic Republic of the Congo (DRC), Nigeria and Morocco in Africa is also the goal of our country's focus and layout.

Based on the domestic, increase the intensity of exploration, rational development and utilization of tin resources: the domestic identified tin resources to carry out protective mining, control the scale of mining, the establishment of a reasonable reserve mechanism; With the domestic supply-side reform and increasing the intensity of environmental protection, there is a great pressure on the supply of domestic mineral products. At present, the state attaches great importance to environmental protection, and for the first time, the state has written "Green Water and Green Mountain is Jinshan Silver Mountain" into the report of the 19th CPC National Congress. With the continuous progress of the construction of ecological civilization, the state has issued a series of environmental protection policies and regulations. The general trend of policy is to strengthen the ecological protection of land and space and raise the entry threshold of land and space development. The number of nature reserves has increased year by year, and the mining rights in nature reserves have been classified and withdrawn one after another, which has brought a certain impact on the domestic mining industry. Therefore, while the mining right withdraws from the nature reserve, we should constantly strengthen the domestic prospecting efforts to ensure the supply of domestic mineral products.

Strengthen recycling: large recycling space, China's recycled tin production reached a peak of more than 40,000 tons in 2010, the output began to decline, in recent years maintained at more than 30,000 tons. Recycled tin accounts for 20% of consumption in China.

Summary: increased demand, limited resources, tight supply, large import uncertainty, long-term price rise.

![The Most-Traded SHFE Tin Contract Opened Sharply Lower in the Night Session and Maintained a Fluctuating Trend at Lows, While Spot Market Transactions Gradually Recovered [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/TMpAM20251217171753.jpg)